Ian Woodward's Investing Blog

Ian Woodward's Investing BlogBulls Live to Fight Another Day

Thursday, November 29th, 2007

The Stock Market has been kind to the Bulls these last three days just when we felt they were down and out for the count. It took new news to get a rally going again, but it is a little too early to call if it will continue into a full-bloodied Santa Claus Rally. Let’s review the bidding:

- We had an oversold market and the Sheiks of Abu Dhabi stepped up to the plate with a $7.5B loan to Citigroup that changed the paradigm for the moment on the Credit Crunch situation. That gave us a relief for the first day to get the Bulls out of the depths of despair. The Bears were taken by surprise and had to run for cover.

- To rub salt in the wounds of the Bears and raise the hopes of the Bulls, it is amazing how the Fed Governors come charging in on their white horse to give a glimmer of hope that they will make a further rate cut at their FOMC Meeting on December 11th. Vice Chairman Donald Kohn hinted as much yesterday and that sent the DOW charging like a Bull in a China Shop for another 300+ point up day, and the shorts having to cover in earnest. Crazy Market…just when the Bears had the end zone in their sights of driving the Bulls into a Bear Market. They will have to wait one more time to get a decent run on the likes of the QIDs and the FXPs, etc.

- It doesn’t matter which side of the market one is on, there is only one word…NIMBLE, or if you snooze you lose. Take the QID as an example which is both a good hedging tool and a shorting instrument, up 12% in a matter of four days, and down 9% in three days, so beware unless this kind of action comes automatically to you. You have to be a day trader in order to take advantage of this kind of volatility, but when one sees 38 million shares traded on the QID as normal these days, this is a whole “New Sport” for the thrill seekers.

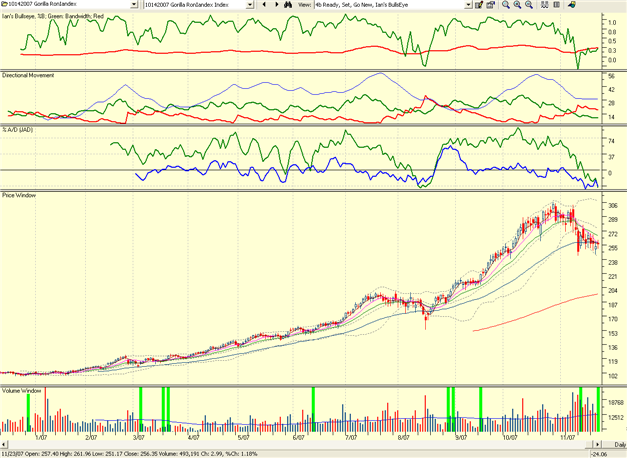

- Of course the action is back into beaten down wolf packs of the likes of Transportation – Shipping, Chemicals – Specialty, or for that matter even the Gorilla RonIandex and Chinese Silverbacks have all found favor again. The Solars are flying high into climax runs, but who cares when everyone is playing the same “Bubble Game”. No such luck for those trying to find a bottom in the Home-builders as they keep inching lower with every fake rally attempt.

- Meanwhile on the Indicator front we have had three

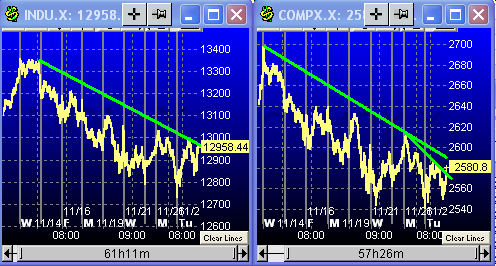

Eureka signals in the span of two weeks, two genuine and one false. The false one is easy to detect in that it was the day after Thanksgiving on November 23, and those should ALWAYS be discounted since they invariably fire on low volume days at holiday time. Yesterday’s signal was definitely one to sit up and taken notice of since it was on heavy volume and had all the trappings of the first day of a true rally if it is to occur. - So now the Bulls wait for the proverbial Follow-through Day, which as the pundits have taught us should occur anytime starting tomorrow through next week…between friends. My last blog gave the conditions both on the DOW and the Nasdaq for the hurdles they had to jump to even begin to consider a Rally ATTEMPT. We are well past the 13,100 and 2640 levels, respectively, so the Bulls can certainly take courage that they have the makings of a Rally attempt. Both Indexes are back to where they were over a week ago, and with today’s pause to refresh there may be a fighting chance of a move to the upside.

- The Ten Year Bond (TNX) is below 4.00 at 3.94 so that is signaling that the bond market, and hence the stock market, is already baking in the expected rate cut in two week’s time. Heaven forbid if that does NOT occur as the Bears will make hay while the sun shines, and will cause all sorts of perturbations prior to the year end.�

So what’s the bottom line of all that? It nets out to two things for the short term:

- Tomorrow being Friday one should expect the decks to be cleared going into the weekend so don’t be surprised to see the market tail off towards the last hour. If not, then it bodes well for the following week.

- Keep a beady eye out for a strong follow through day…if that doesn’t materialize then the obvious conclusion is that we will head down again to test the recent lows and one should look for either a double bottom or a further deterioration into a full blooded Intermediate Correction as the next step. I’m sure you have printed out the stakes in the ground so the game plan is at your elbow and you are all set for whatever the market does. Don’t second guess and wish it to do what you want it to do.�

For the longer term, we should recognize that if we finish up with a Santa Claus rally the Bulls would have dodged two bullets within the span of five months and the long bull rally will now be into a fresh year. We should expect some more dramatic form of correction as by then we can well expect the clamor of Recession showing its ugly head in the Financial Media, especially if the 4th qtr earnings turn out to be disappointing. But that is a story for another day! Best regards, Ian.